Too Much of a Good F(Li)ng

Too Much of a Good F(Li)ng

MSDExtra for February 3 2023

Before I begin with the headline editorial of this installment of MSDExtra, let me address a couple items.

Yes, I understand its been 1 month+ since the last installment of MSDExtra. Writing is hard. I have mad respect for those newsletter writers who can pump out a couple pages each trading day. Thats a skill few have.

Since the holidays we also launched 3 news podcasts from ClearComm. We now have our first episodes focused on oil/gas, uranium and battery metals. We are currently locking in episode 2 for each to be aired this month. We’d appreciate you following and perhaps event constructively reviewing.

I invite you to visit the new ClearComm website!

Now to the business at hand…

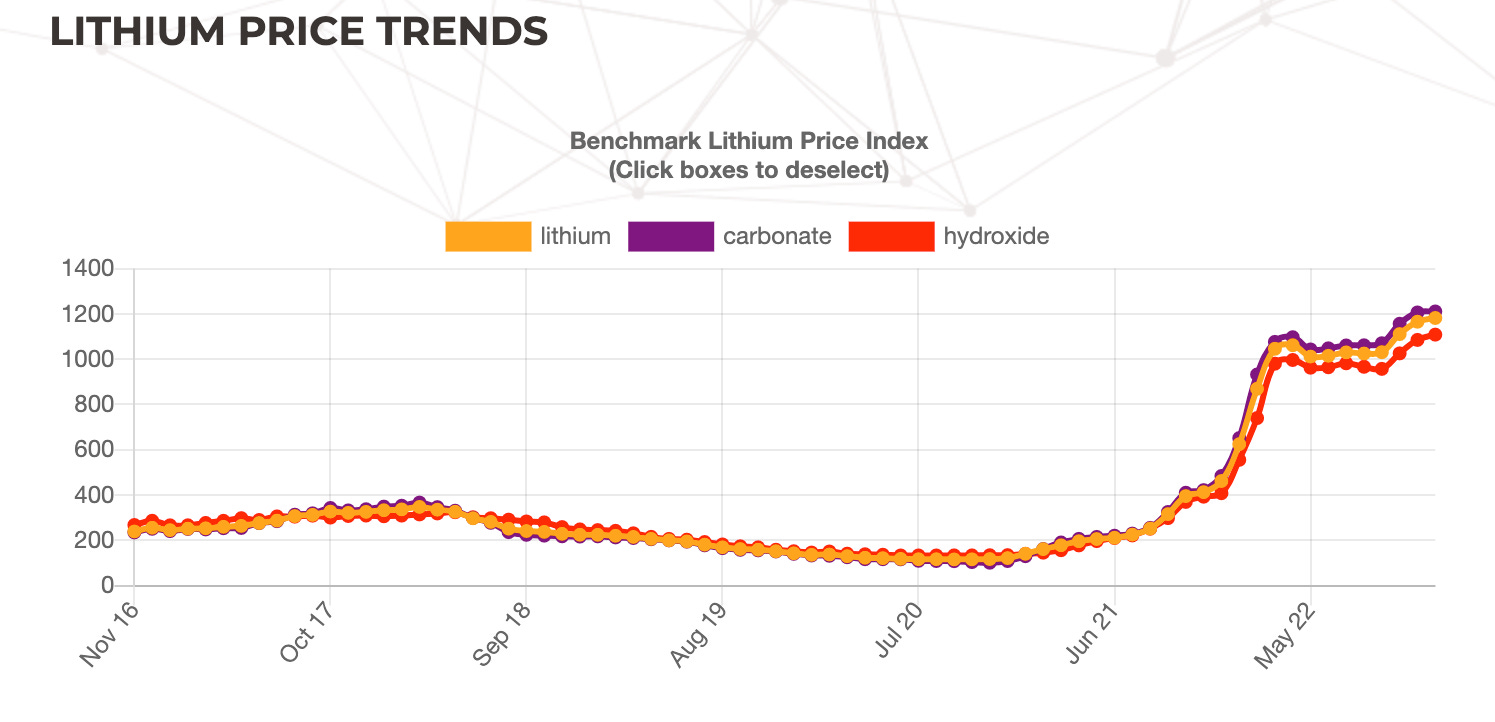

Late in 2022 I wrote a snippet editorial on the lithium price. At the time, the prices (carbonate, hydroxide, etc) soared but it looked like it could go higher. It did exactly that in the last few weeks of the year. Let’s take a quick look at the Benchmark Metals Lithium Index for visual representation of the price action.

Can the lithium price go higher? Your guess is as good as mine. However, I’m under the impression that it does NOT need to go higher. Current producing lithium mines don’t need this high of price to make them economic. In fact, you could cut the lithium price in half and good projects still are raking in serious margins.

I’m not a lithium expert, by any means! (I’ll leave that stuff to Chris Berry!) But I can see sentiment percolating quite a bit, and this is what I want to focus on.

In October 2022, prices for battery grade lithium carbonate in China hit an all-time high of $74,475 per tonne. The speculation in lithium carbonate has certainly become frothy. I understand there are fundamentals of supply/demand, EVs, battery technology, etc underlying the price moves. However, this jumped out at me earlier this week when I reported American Lithium’s Preliminary Economic Assessment highlights:

American Lithium is using a $20,000/tonne base case for their technical report. Current prices are nearly 3X that. I suppose I should say kudos for being incredibly conservative in the sensitivity table.

And lithium speculation is pushing lithium equities to the stratosphere. Take a look at a few of these charts, including our beloved Patriot Battery Metals (which I still own a VERY small amount of shares because I just keep selling into this rally).

Tearlach Resources jumped into the lithium space in 2022. Here’s what happened with their share price.

Brunswick Exploration has been acquiring more lithium exploration ground in Quebec, Manitoba and Saskatchewan over the past year. Not much in regards to results since then. Here’s how they have traded.

Also in Quebec, Critical Elements is advancing the Rose project. They published a technical report back in June. But in regards to news, nothing of big substance since November. Yet, their share price has surged.

But my favorite sentiment indictor comes from the former explorer known as Madi Minerals. The company amalgamated with Casey Jones Lithium in August and recently renamed themselves “Pegmatite One Lithium and Gold.”

Sentiment appears to have gotten out of hand. The indicators are all out there and it follows every other sentiment cycle in the metals space. First, the metal itself gets bid up on speculation, then the producing equities, followed by the junior exploration equities, and then the name changes with a heavy dose of new listings related to the metal.

Four checkmarks.

Time for correct.

And if you are fortunate to enjoy the ride, well, you never go broke taking profits.

Could the lithium equities continue its rise? Perhaps for a bit longer, but at at this point the technicals do not represent the fundamentals. Speculation has a tight grip on this market. And it will, until it doesn’t.

As Jared Dillian reminds us, what is unsustainable cannot be sustained. Folks, 5X returns on little news is unsustainable.

Time to take Lithium “Back to the Middle”

Back to the middle

This is where love has left me

It's an endless cycle

Please don't take it away from me

Thank you to our Partners